What you see on the quote and what your wallet actually receives are two different numbers. The gap is the routing tax.

There are three taxes on every on-chain trade. You only see one.

You sign a swap. The interface quoted 24,950 USDC. You confirm. The wallet pings. You check the explorer. You actually received 24,160.

Eight hundred and thirty dollars vanished somewhere between the quote and the fill. The interface does not explain where. The block explorer does not explain where. You shrug, blame slippage, and move on with your day.

Most of that money did not go to the protocol. It did not go to the network. It went to a constellation of small mechanisms that quietly tax every transaction touching public liquidity. Understanding those mechanisms is the difference between a trader who keeps four-fifths of their alpha and a trader who hands it away to bots and bad routing. This is the same problem a modern AI-powered trading aggregator is built to solve, and it is worth walking through the math of it from scratch.

There are three taxes. The trader sees one. Pays all three.

Tax #1: slippage and the math of a single pool

Slippage is the gap between the price you expected and the price you got. The reason it exists is geometric. AMM-style liquidity pools price assets along a bonding curve, which means the more of one side you buy, the more expensive the next unit becomes. A $200 swap barely moves the curve. A $20,000 swap pushes it noticeably. A $200,000 swap can bend the curve so hard that your last dollar pays substantially more per token than your first.

Here is the part that surprises most retail traders. Slippage scales with the ratio of order size to pool depth, not with order size in absolute terms. A $5,000 order in a $50,000 pool is brutal. The same $5,000 order in a $50 million pool is invisible. Same money. Completely different outcome. The pool you happened to land on matters more than the price you happened to see.

This is why a thoughtful trader cares about pool depth before they care about quoted price. The quote is a snapshot. The fill is a function. And a function that depends on pool size will always punish anyone who routed into the wrong pool, regardless of how good the quote looked at signing time.

Order size is the lever the trader controls. Pool selection is the lever the router controls. If you do not have a router doing that work, you are the router. Most retail traders are routers who do not know they are routers, and they are not very good at it.

Tax #2: MEV and the bots that watch your transactions before they happen

This one is darker, more profitable for the people running it, and worth slowing down on.

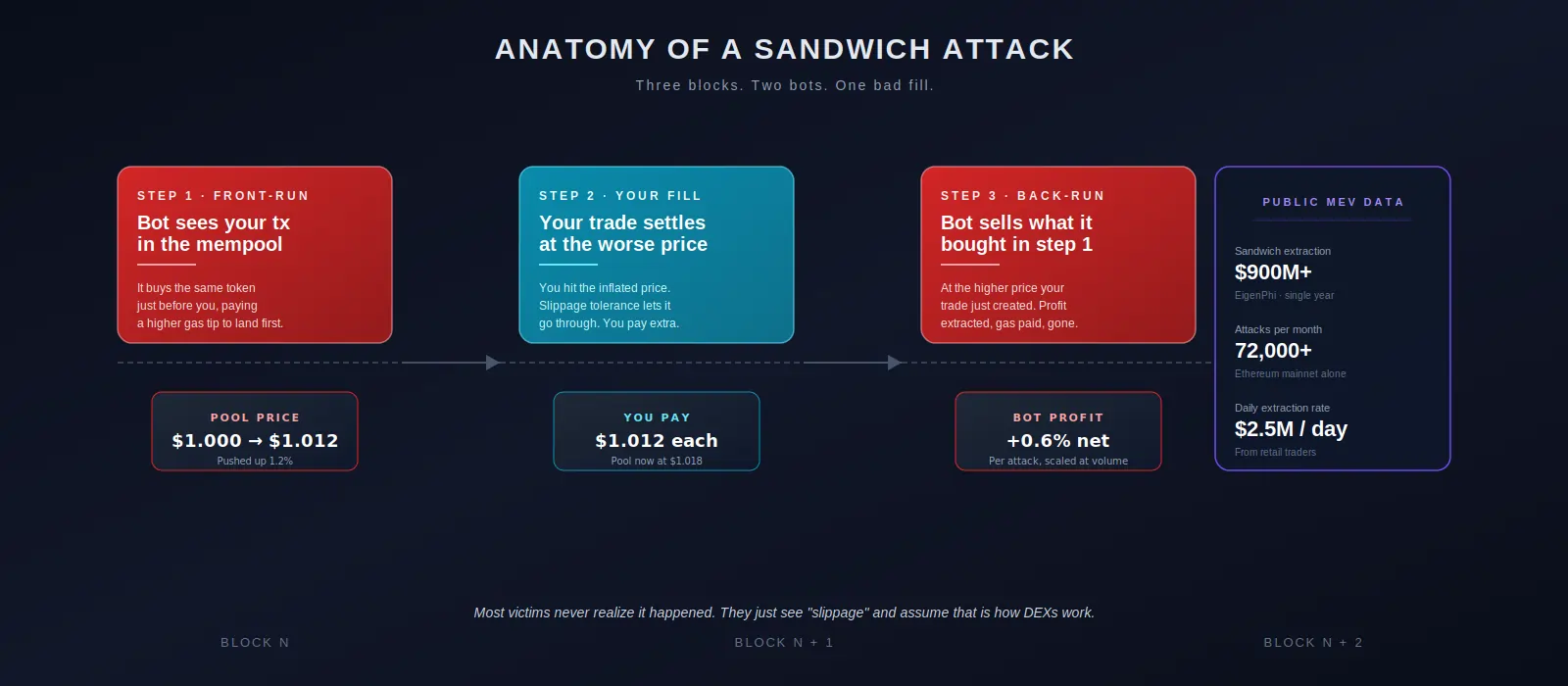

Maximum Extractable Value (MEV) is value that can be captured by reordering, inserting, or censoring transactions inside a block. The most common form of MEV that touches retail is the sandwich attack. Searchers running specialized bots monitor the public mempool, spot a pending swap that will move the price, and squeeze a trade in on either side of it.

The mechanics, step by step. A bot sees your transaction sitting in the mempool. It estimates the price impact your trade will have. If the math works, it sends two transactions: one before yours (a buy) and one after yours (a sell). It pays extra gas to make sure its first transaction lands ahead of yours. The bot’s buy pushes the price up. Your trade fills at the now-inflated price, which your slippage tolerance allows. The bot’s sell happens at the new higher price. The profit difference is taken from your fill.

Most victims never realize it happened. They see slippage that is slightly worse than expected, blame it on volatility, and move on. The number who realize they were sandwiched is a tiny fraction of the number who actually were.

The scale here is not small. Independent MEV researcher EigenPhi has documented over 900 million dollars extracted from DeFi users through sandwich attacks across a single year. On Ethereum alone, public dashboards have tracked more than 72,000 sandwich attacks in a single 30-day window, with over 35,000 distinct victims. That works out to roughly 2.5 million dollars per day of value siphoned off retail traders. Per day.

Three blocks, two bots, one bad fill. The user sees ordinary slippage. The data behind the scenes tells a different story.

The defenses against sandwich attacks exist. Private mempools, where transactions are not broadcast publicly. Tight slippage tolerances, which sometimes cause failed trades but cap the maximum extractable amount. Intent-based architectures, where the trader signs an intent and a solver fulfills it, so the trader is never the one in the public mempool being watched.

And mempool-aware routing, where an execution layer watches the same data the bots are watching, detects sandwich attempts forming around your transaction, and reroutes or delays the fill before the attack can land. That last one is the only defense that scales without requiring the trader to manage anything manually. It is also the layer most retail traders do not realize they should be looking for.

Tax #3: gas, bridge fees, and the costs that look small until you add them up

This is the visible cost. The one everyone knows about. Which is exactly why it gets undertreated.

Gas is the fee you pay the network to include your transaction. On busy chains during congestion, gas spikes can turn a $4 transaction into a $90 transaction. Priority fees, which buy your transaction faster inclusion, layer on top. Bridge fees apply when assets move between chains. None of these are predatory like MEV. They are the price of using the infrastructure.

But the route choice still matters here. A swap that hits three pools on one chain pays gas three times. A cross-chain trade pays gas on both chains plus a bridge fee. A route through a popular pool during peak congestion pays more gas than the same route during a quiet hour. The cumulative impact of bad route selection can easily multiply your effective network cost by three or four times.

A good router does not eliminate these costs. Nothing can. But it folds them into the displayed price before you sign, which means there are no nasty surprises after the fact, and it picks the path that minimizes them given current network conditions. That alone often recovers 0.3 to 0.6% on a typical mid-size swap, which compounds across a year of trading into real money.

Where each cost hides

| Cost | Where it lives | Who pays it |

|---|---|---|

| Slippage | Inside the pool’s bonding curve. The bigger your order relative to pool depth, the worse the math | Anyone who hits a single venue with a non-tiny order. Whales feel it most. Retail still bleeds quietly |

| MEV / sandwich | In the mempool, between submission and inclusion. Bots reorder transactions for profit | Anyone using a public mempool without MEV defense. Retail is sandwiched at higher rates than they realize |

| Gas + bridge fees | On-chain transaction fees, plus any bridging cost if the trade crosses networks | Everyone, on every transaction. Cannot be eliminated, only minimized by smart route choice |

How smart liquidity routing actually cuts costs one and two

Now we get to the part that matters. There are three taxes. The third is mostly inevitable. The first two are largely solvable, and they are solvable by the same primitive: a routing layer that knows more about liquidity than you do.

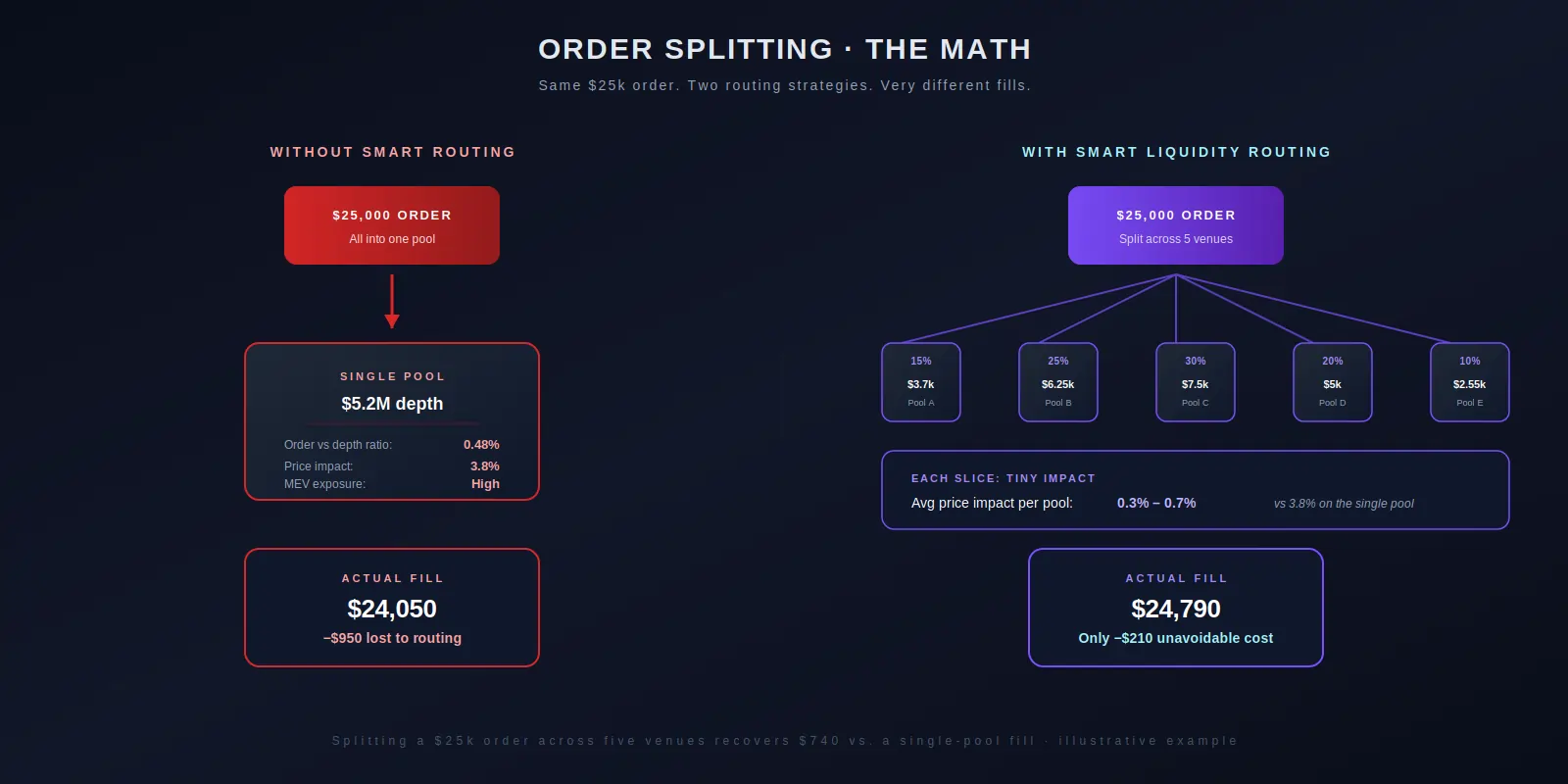

The core idea behind smart liquidity routing is straightforward. Instead of sending your whole order to one pool and hoping for the best, the router treats your order as a problem to be optimized across every reachable pool simultaneously. It models price impact at each venue based on current depth. It models gas cost per route. It scans for MEV exposure on each path. Then it splits the order, sometimes across three pools, sometimes across eight, in whatever proportions minimize the total cost of execution.

The math is more elegant than it looks. If your order would cost 3.8% in price impact going into a single pool, but you split it 30/25/20/15/10 across five venues, each slice pays the impact for its smaller size against that specific pool’s depth. The largest slice pays maybe 1.0%. The smallest pays 0.2%. The blended cost lands somewhere around 0.6 to 0.8%, depending on how the depths line up.

Add MEV defense to that. The router watches the mempool while it is building the route. If it sees sandwich patterns forming around the venues it was about to send slices to, it can switch venues, throttle the slippage parameter, or delay the transaction by a block. The trader never sees any of this. The trader sees a clean fill that is closer to the quote than they expected.

Illustrative comparison. Splitting a single $25k order across five venues cuts the cumulative price impact roughly in half compared to dumping the whole order into one pool.

This is also why aggregation matters more, not less, as order size grows. A $500 swap fills cleanly almost anywhere. A $50,000 swap behaves like a moving truck on a narrow road if you put it all into one pool. Smart routing turns that moving truck into five smaller vans that each take a different street. Same destination. Wildly different cost.

Manual single-pool trade vs. smart-routed trade

| $25k swap (illustrative) | Manual single-pool execution | Smart-routed execution |

|---|---|---|

| Routing | One venue, often the one the wallet remembers from your last swap | Order sliced across multiple pools sized to absorb each slice without moving the price |

| Price impact | Roughly 2 to 4% on a mid-cap pair with $5M of pool depth | Roughly 0.3 to 0.7% per slice, blended out to under 1% total |

| MEV exposure | Fully exposed unless the user manually configures a private RPC | Mempool monitored, route or slippage parameter adjusted on the fly, sandwich attempts dodged |

| Contract risk | Trader’s responsibility to vet, usually skipped on familiar-looking tokens | Honeypot, blacklist, and rug patterns scanned before the route is even built |

| Custody | Varies, often custodial if routed through a CEX-flavored UI | Non-custodial throughout, assets never leave the user’s wallet during routing |

| Net delta on the fill | Receives approximately $24,050 (illustrative) | Receives approximately $24,790 (illustrative). Difference: ~$740 retained |

What an AI-driven execution core adds on top of smart routing

Smart routing is the floor. The ceiling involves an additional layer that watches more than just liquidity.

An AI-driven execution core does real-time analysis of markets, liquidity, and the smart contracts your transaction is about to touch. Liquidity fragmentation, intra-block volatility, and contract integrity are checked at the moment the route is built, not pulled from a stale cache. This matters because the optimal route on Tuesday at noon is not the optimal route on Tuesday at 9pm when a token’s main pool just had a 40% withdrawal.

On top of that sits the contract scanning layer. Honeypots. Tokens whose contract lets the deployer drain the pool. Tokens with hidden transfer taxes. Tokens with blacklist functions that turn the buy side into a one-way ticket. Recently upgraded contracts whose new admin keys point to a fresh wallet. A well-built AI protection layer flags these before the trader ever signs, which is genuinely the difference between a slippage event (annoying) and a total loss (catastrophic).

The other part worth flagging is custody. Routing layers vary on this. Some take custody of funds during the route. Some do not. A non-custodial trading aggregator keeps assets in the user’s wallet for the entire flow, which means even if the routing layer goes down, gets compromised, or simply makes a mistake, the trader’s funds are not at risk in the same way they would be on a custodial platform. This is not a marketing point. It is a structural property that determines how bad a bad day can get.

A practical pre-trade checklist

Before you sign a swap above the size where slippage starts to matter (call it $1,000 and up, lower if you trade often), it is worth running through a few questions. None of them require deep expertise. All of them save real money over time.

- Is this swap going through one pool or multiple? If one, what is the depth of that pool relative to your order size?

- What is your slippage tolerance set to? Anything above 1% on a major-pair swap is an invitation to bots.

- Is the displayed quote inclusive of gas and any bridge fees, or are those going to surface after you sign?

- Has the contract you are interacting with been deployed recently or upgraded recently? If yes, dig before signing.

- Is this transaction going to broadcast through a public mempool, or is there a private channel option?

- Is the platform you are using non-custodial all the way through, or does it briefly take custody during routing?

- If you cannot answer the above for the platform you use, that is a useful signal in itself.

The simple takeaway

On-chain trading is not free. It was never free. The fees are simply distributed in ways that most interfaces do not show you.

Slippage compounds across every trade you make. MEV extraction is industrial-scale and most of its victims do not know they were victims. Gas and bridge fees are visible but still influenced by route quality. The trader who pays attention to these three taxes, and uses execution infrastructure built to minimize them, runs at a structural advantage over the trader who clicks Swap and hopes.

That advantage compounds. Two percent saved per swap, across a hundred swaps a year, is not a rounding error. It is the difference between an okay year and a memorable one.