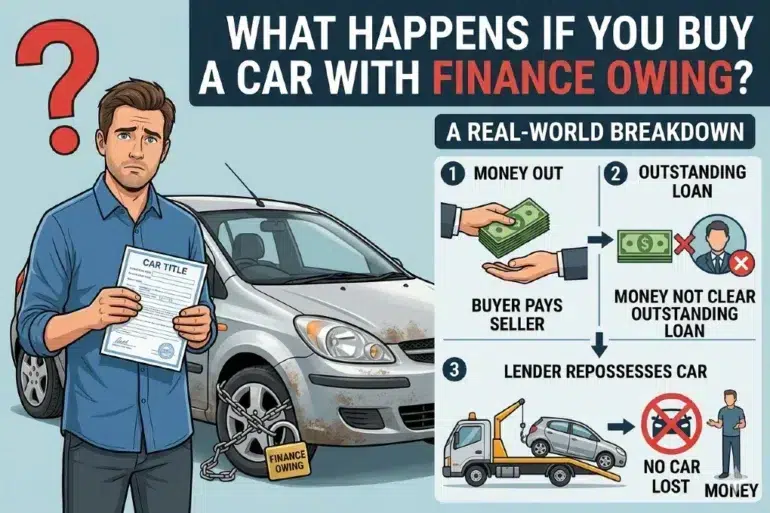

Buying a used car can feel like a win—especially when you find one that looks great, drives well, and fits your budget. But there’s a hidden risk that many buyers don’t think about until it’s too late: outstanding finance.

In simple terms, this means the previous owner still owes money on the car. And while that might sound like their problem, it can quickly become yours.

Let’s break down what actually happens in real life when you unknowingly buy a car with finance owing—and how you can avoid a situation that could cost you thousands.

The Hidden Problem Behind a “Good Deal”

Imagine this: you find a car listed online at a price that’s just a little lower than similar models. The seller seems genuine, the car looks clean, and everything checks out during your test drive.

You agree on the price, pay in cash or bank transfer, and drive home feeling like you’ve scored a great deal.

But a few weeks later, you receive a call—or worse, a visit—from a finance company. They inform you that the car still has a loan attached to it, and the previous owner has stopped making payments.

Here’s the part that surprises most people:

the debt is tied to the car, not the person.

That means the lender still has a legal claim over the vehicle—even though you’ve already paid for it.

Can the Car Really Be Taken Back?

Short answer: yes.

If a car has outstanding finance, it’s considered secured debt. This means the lender used the car itself as collateral for the loan. If the borrower fails to repay, the lender has the legal right to repossess the vehicle.

So even if you:

- Bought the car in good faith

- Paid the full amount

- Had no idea about the finance

…the lender can still take the car back.

And unfortunately, you usually won’t get your money back from them. Your only option would be to chase the seller—who may no longer be reachable.

A Real-World Scenario

Let’s look at a common situation.

Mark, a small business owner, needed a second vehicle for deliveries. He found a used van online at a great price and bought it from a private seller. Everything seemed fine—until two months later, when the van was repossessed due to unpaid finance.

Mark lost the van and the money he paid for it.

For him, this wasn’t just an inconvenience—it affected his business operations, delayed deliveries, and cost him additional money to replace the vehicle.

This kind of situation doesn’t just happen to individuals. It can impact:

- Families buying their first car

- Students looking for budget transport

- Tradies purchasing second-hand tools or vehicles

- Businesses investing in used equipment

The consequences go beyond financial loss—they disrupt daily life and work.

Why It Happens More Often Than You Think

You might assume this kind of situation is rare, but it’s actually more common than people realize.

Here’s why:

- Private sales don’t always include full transparency

Sellers may forget, ignore, or deliberately hide the fact that money is still owed. - Cars are frequently used as loan security

Many car loans are secured against the vehicle itself. - Buyers rely on trust instead of verification

A friendly seller and a smooth transaction can give a false sense of security.

In other words, it’s not always about scams. Sometimes it’s just a lack of proper checks.

How to Protect Yourself Before Buying

The good news is that this situation is completely avoidable with one simple step: checking the vehicle’s history before you buy.

This is where doing your due diligence really pays off.

Before handing over any money, take the time to verify:

- Whether the car has outstanding finance

- If it’s been reported stolen

- Whether it has been written off in the past

One of the easiest ways to do this is to search vehicle history in Australia

This type of check uses the car’s unique identifier (called a VIN, or Vehicle Identification Number) to pull up important records linked to the vehicle.

Think of it like a background check—not on the seller, but on the car itself.

What a Simple Check Can Save You

Spending a small amount of time (and a small fee) on a vehicle history check can save you from:

- Losing thousands of dollars

- Having your car repossessed

- Dealing with legal complications

- Experiencing stress and uncertainty

It also gives you peace of mind, knowing that the car you’re buying is truly yours—free and clear.

In many ways, it’s similar to buying a house. You wouldn’t purchase property without checking for existing debts or legal issues. The same logic applies here.

Final Thoughts: A Small Step That Makes a Big Difference

Buying a used car should be an exciting experience—not a stressful one.

But as we’ve seen, skipping a simple check can turn a good deal into a costly mistake. The reality is that outstanding finance isn’t always visible, and relying on trust alone just isn’t enough.

By taking a few extra minutes to verify a vehicle’s history, you’re protecting not just your money, but your time, your plans, and your peace of mind.

Because at the end of the day, the goal isn’t just to buy a car—it’s to own it with confidence.